As filed with the Securities and Exchange Commission on August 4, 2023.

Registration Statement No. 333-267328

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Post-Effective Amendment No. 2 to

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

XORTX THERAPEUTICS INC.

(Exact name of registrant as specified in its charter)

| British Columbia (State or other jurisdiction of incorporation or organization) | 2834 (Primary Standard Industrial Classification Code Number) | N/A (I.R.S. Employer Identification No.) |

3710 – 33rd Street

NW

Calgary, Alberta, Canada T2L 2M1

(403) 455-7727

(Address, including zip code and telephone number, including area code, of registrant’s principal executive offices)

C T Corporation

1015 15th Street N.W., Suite 1000

Washington, D.C., 20005

(202) 572-3133

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Thomas M. Rose Troutman Pepper Hamilton Sanders LLP 401 9th Street, N.W., Suite 1000 Washington, DC 20004 (202) 274-2950 | Rick Pawluk Fasken Martineau DuMoulin LLP 350 7th Avenue SW, Suite 3400 Calgary AB T2P 3N9 Canada (587) 233-4063 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act.

Emerging growth company x

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.† ¨

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

This Post-Effective Amendment No. 2 relates to the Registration Statement on Form F-1 (File No. 333-267328) (the “Registration Statement”) of XORTX Therapeutics Inc. (the “Company”) originally declared effective by the U.S. Securities and Exchange Commission (“SEC”) on September 22, 2022 (the “Initial Registration Statement”).

The Company is filing this Post-Effective Amendment No. 2 to the Initial Registration Statement (i) to incorporate by reference into the Registration Statement the Company’s Annual Report on Form 20-F for the year ended December 31, 2022, filed with the SEC on April 28, 2023, (ii) to incorporate by reference into the Registration Statement the Unaudited Condensed Interim Consolidated Financial Statements for the three months ended March 31, 2023 and 2022 and the Management Discussion and Analysis for the three months ended March 31, 2023, filed as Exhibits 99.1 and 99.2, respectively, to our Report on Form 6-K furnished to the SEC on May 16, 2023, (iii) to incorporate by reference the Company’s Forms 6-K filed on May 24, 2023, May 30, 2023 and June 30, 2023, and (iv) to include certain other information in the Registration Statement. This Post-Effective Amendment No. 2 contains an updated prospectus relating to the offer and sale of the Company’s common shares issuable upon the exercise of warrants as described herein.

No additional securities are being registered pursuant to this Post-Effective Amendment No. 2.

All filing fees payable in connection with this Registration Statement were paid by the Company at the time of filing of the Initial Registration Statement.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED AUGUST 4, 2023

PRELIMINARY PROSPECTUS

5,000,000 Common Shares Issuable upon

Exercise of Warrants

XORTX Therapeutics Inc.

We are offering 5,000,000 common shares issuable upon exercise of 5,000,000 common share purchase warrants (the “Warrants”) pursuant to this prospectus. The Warrants were offered and sold by us pursuant to a prospectus dated October 4, 2022 as part of a public offering of common share units and pre-funded warrant units. The common share units consisted of 1,400,000 common shares and Warrants to purchase up to 1,400,000 common shares. The pre-funded warrant units consisted of 3,600,000 pre-funded warrants and Warrants to purchase up to 3,600,000 common shares. The common shares and Warrants were immediately separable upon issuance. Each common share unit was sold at a price of $1.00 per common share unit. Each pre-funded warrant unit was sold at a price of $0.9999 and had an exercise price of $0.0001. The Warrants sold in the offering have an exercise price of $1.22 and expire five years from the original date of issuance (October 7, 2027). No securities are being offered pursuant to this prospectus other than the common shares that will be issued upon the exercise of the Warrants.

In order to obtain the common shares offered hereby, holders of Warrants must pay the applicable exercise price per Warrant. We will receive proceeds from the exercises of the Warrants for cash, if any, but not from the sale of the underlying common shares.

There is no established public trading market for the Warrants, and we do not expect a market to develop. In addition, we do not intend to apply for the listing of the Warrants on any national securities exchange. Without an active trading market, the liquidity of the Warrants will be limited.

Our common shares are currently traded under the symbol “XRTX” on the TSX Venture Exchange (the “TSXV”) and on the Nasdaq Capital Market (“Nasdaq”).

We are an “emerging growth company” as defined by the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and, as such, we have elected to comply with certain reduced public company reporting requirements for this prospectus and future filings. However, we have elected not to take advantage of the extended transition period allowed for emerging growth companies for complying with new or revised accounting guidance as allowed by Section 107 of the JOBS Act and Section 7(a)(2)(B) of the Securities Act of 1933, as amended, (the “Securities Act”).

Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 10.

We are a “foreign private issuer” as defined under the federal securities laws and, as such, are subject to reduced public company reporting requirements. See “Prospectus Summary – Implications of Being a Foreign Private Issuer.”

Neither the Securities and Exchange Commission, Canadian securities commission nor any domestic or international securities body has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Prospectus dated , 2023

This prospectus is part of a registration statement on Form F-1 that we filed with the Securities and Exchange Commission (“SEC”).

You should read this prospectus and the related registration statement carefully. This prospectus and registration statement contain important information you should consider when making your investment decision. See “Where You Can Find More Information” in this prospectus.

We have not authorized anyone to provide you with information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give to you. The information contained in this prospectus or any free writing prospectus is accurate only as of the date of this prospectus or such free writing prospectus, regardless of the time of delivery of this prospectus or any free writing prospectus.

We are offering to sell, and seeking offers to buy, securities only in jurisdictions where offers and sales are permitted. We have not taken any action to permit a public offering of our securities or the possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourself about and to observe any restrictions relating to this offering and the distribution of this prospectus.

We express all amounts in this prospectus in United States dollars, except where otherwise indicated. References to “$” are to United States dollars and references to “CAD$” are to Canadian dollars.

Except as otherwise indicated, references in this prospectus to “XORTX,” the “Company,” “we,” “us” and “our” refer to XORTX Therapeutics Inc. and its consolidated subsidiaries.

1

This summary highlights certain information contained elsewhere in this prospectus. This summary does not contain all of the information that may be important to you. You should read and carefully consider the following summary together with the entire prospectus, including all documents incorporated by reference herein. In particular, attention should be directed to the “Risk Factors,” beginning on page 10 of this prospectus and to the sections “Risk Factors,” “Information on the Company,” “Operating and Financial Review and Prospects” and the financial statements and related notes thereto incorporated by reference hereto, in our Annual Report on Form 20-F for the fiscal year ended December 31, 2022, before making an investment decision. See also “Cautionary Note Regarding Forward-Looking Statements,” “Incorporation by Certain Information by Reference” and “Where You Can Find Additional Information” in this prospectus.

Overview

XORTX Therapeutics is a late stage clinical pharmaceutical company focused on identifying, developing and potentially commercializing therapies to treat progressive kidney disease modulated by aberrant purine and uric acid metabolism in orphan (rate) disease indications such as autosomal dominant polycystic kidney disease (“ADPKD”) and type 2 diabetic nephropathy (“T2DN”), as well as acute kidney injury (“AKI”) associated with respiratory virus infection.

Our focus is on developing three therapeutic product candidates to:

| · | slow or reverse the progression of chronic kidney disease in patients at risk of end stage kidney failure; |

| · | address the immediate need of individuals facing AKI associated with respiratory virus infection; and |

| · | Treat patients with type 2 diabetic nephropathy. |

We are also looking to identify other opportunities where our existing and new intellectual property can be leveraged to address health issues.

We believe that our technology is underpinned by well-established research and insights into the underlying biology of aberrant purine metabolism, its health consequences and of oxypurinol, a uric acid lowering agent that works by effectively inhibiting xanthine oxidase. We are developing innovative product candidates that include new or existing drugs that can be adapted to address different disease indications where aberrant purine metabolism and/or elevated uric acid is a common denominator, including polycystic kidney disease, pre-diabetes, insulin resistance, metabolic syndrome, diabetes, diabetic nephropathy, and infection. Oxypurinol, and our proprietary pipeline-in-a-product strategy supported by our intellectual property, established exclusive manufacturing agreements, and proposed clinical trials with experienced clinicians, are focused on building a pipeline of assets to address the unmet medical needs for patients with a variety of serious or life-threatening diseases:

| · | XRx-008, a program for the treatment of ADPKD; |

| · | XRx-101, a program to treat AKI associated with severe respiratory infection and associated health consequences; and |

| · | XRx-225, a program for the treatment of T2DN. |

At XORTX, we aim to redefine the treatment of kidney diseases by developing medications to improve the quality-of-life of patients with life threatening diseases by modulating aberrant purine and uric acid metabolism, including lowering elevated uric acid as a therapy.

Our Proprietary Therapeutic Programs

Our expertise and understanding of the pathological effects of aberrant purine metabolism combined with our understanding of uric acid lowering agent structure and function, has enabled the development of our proprietary therapeutic platforms. These are a complementary suite of therapeutic formulations designed to provide unique solutions for acute and chronic disease. Our therapeutic platforms can be used alone, or in combination, with synergistic activity to develop a multifunctional tailored approach to a variety of disease entities that can address disease in multiple body systems through management of chronic or acute hyperuricemia, immune modulation, and metabolic disease. We continue to leverage these therapeutic platforms to expand our pipeline of novel and next generation drug-based product candidates that we believe could represent significant improvements to the standard of care in multiple acute and chronic cardiovascular diseases and specifically kidney disease.

2

We believe our in-house drug design and formulation capabilities confer a competitive advantage to our therapeutic platforms and are ultimately reflected in our programs. Some of these key advantages are:

Highly modular and customizable

Our platforms can be combined in multiple ways and this synergy can be applied to address acute, intermittent or chronic disease progression. For example, our XRx-101 program for AKI is designed to produce rapid suppression of hyperuricemia then maintain purine metabolism at a low level during viral infection and target management of acute organ injury. Our XRx-008 program is designed for longer term stable chronic oral dosing of xanthine oxidase inhibitors. We believe the capabilities of our formulation technology allow us to manage the unique challenges of cardiovascular and renal disease by modulating, purine metabolism, inflammatory and oxidative state.

Fit-for-purpose

Our platforms can also be utilized to engineer new chemical entities and formulations of those agents that have enhanced properties. For example, our XRx-225 product candidate program, some of the intellectual property for which we license from third parties, represents a potential new class of xanthine oxidase inhibitor with a targeted design to enhance anti-inflammatory activity. The capability of tailoring the potential therapeutic benefit of this class of new agents permits us to identify targets and disease that we wish to exploit and then through formulation design optimize those small molecules and proprietary formulations to maximize potentially clinically meaningful therapeutic effect.

Readily scalable and transferable

Our in-house small molecule and formulations design expertise is positioned to create a steady succession of product candidates that are scalable, efficient to manufacture (by us or a partner or contract manufacturing organization), and produce high production and high purity active pharmaceutical drug product. We believe this will provide a competitive advantage, new intellectual property and opportunity to provide first-in-class products that target unmet medical needs and clinically meaningful quality of life.

Our team’s expertise in uric acid lowering agents, specifically in the development and use of xanthine oxidase inhibitors, has enabled the development of our therapeutic product candidates to treat the symptoms of, and potentially delay the progression of ADPKD, AKI due to respiratory virus infection, and T2DN. There is no guarantee that the Food and Drug Administration (“FDA”) will approve our proposed uric acid lowering agent product candidates for the treatment of kidney disease or the health consequences of diabetes.

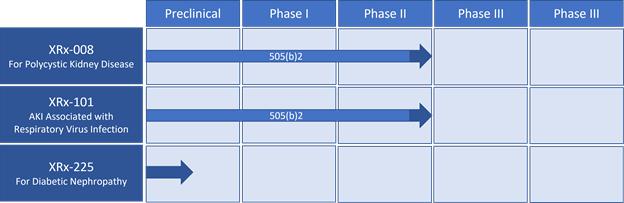

Product Candidate Pipeline

Our lead product candidates are XRx-008, XRx-101, and XRx-225. XRx-008 is in preparations for a Phase 3 registration clinical trial, the last stage of clinical development before application for FDA approval. Our XRx-101 program is advancing toward preparing for a “bridging” pharmacokinetic study for the Company’s Phase 3 clinical trial to potentially slow or reverse acute kidney disease in hospitalized individuals with respiratory virus infection. XRx-225 is at the non-clinical stage and advancing toward the clinical development stage.

Products

The Company’s most advanced development program, XRx-008, sometimes referred to by its trademarked name XORLOTM, is a late clinical stage program focused on demonstrating the potential of our novel product candidate for ADPKD. XRx-008 is the development name given to XORTX’s proprietary oral formulation of oxypurinol, and shows increased oral bioavailability compared to oxypurinol alone. XORTX is also developing a second proprietary combination product composed of a uric acid lowering agent administered intravenously, followed by a xanthine oxidase inhibitor - XRx-101 -, for use in treating patients hospitalized with respiratory virus infection and accompanying hyperuricemia with associated AKI.

XORTX is currently evaluating xanthine oxidase inhibitor candidates for the XRx-225 program to potentially treat T2DN as well as developing new chemical entities to address the large unmet medical need.

Patents

XORTX is the exclusive licensee of two U.S. granted patents with claims to the use of all uric acid lowering agents to treat insulin resistance or diabetic nephropathy, and two U.S. patent applications with similar claims for the treatment of metabolic syndrome, diabetes, and fatty liver disease. Counterparts for some of these patent applications have also been submitted in Europe. In both the US and Europe, XORTX owns composition of matter patent applications for unique proprietary formulations of xanthine oxidase inhibitors – U.S. and European patents have been granted. XORTX has also submitted two patent applications to cover the use of uric acid lowering agents for the treatment of the health consequences of respiratory virus infection.

3

XORTX Therapeutics Pipeline:

XORTX has held discussions with the FDA, regarding developing oxypurinol using the 505(b)(2) pathway and right of reference to the former oxypurinol New Drug Application (“NDA”). Those discussions indicated that XORTX has the ability to use existing clinical data to bypass conducting a number of its own Phase 1 and Phase 2 studies for XRx-008 and XRx-101 programs. However, we may elect to conduct our own Phase 1 and Phase 2 studies as necessary or required to gain marketing approval in the aforementioned programs.

Our Strategy

Our goal is to apply our interdisciplinary expertise and pipeline-in-a-product strategy to further identify, develop and commercialize novel treatments in renal disease and indications related to health consequences associated with ADPKD. To achieve this objective, we intend to pursue the following strategies:

| 1. | Subject to discussions with FDA, submit an NDA to the FDA following the successful completion of the Phase 3 clinical registration trial of the XRx-008 product candidate program in order to establish a new standard of care for ADPKD. |

| 2. | Maximize the potential of the XRx-008 product candidate program, if approved, through independent commercialization and through opportunistic collaborations with third parties. |

| 3. | Leverage our pipeline-in-a-product strategy, developing additional proprietary formulations leveraging our experience selecting renal indications and complementing our developments through acquisitions or in-licensing opportunities in nephrology and diabetes when opportunities arise. |

For the balance of 2023, XORTX will continue its focus on advancing XORLOTM as part of the XRx-008 program for ADPKD into a Phase 3 registration clinical trial, initiation of special protocol assessment (“SPA”) discussions with the FDA and initiation of pre-commercialization studies to prepare for potential approval of XORLOTM as well as advancing research in other kidney disease applications. To achieve these objectives, XORTX’s action plan includes:

| 1. | Initiate the Phase 3 clinical trial, XRX-OXY-301, to support an application for “Accelerated Approval” of XORLOTM for individuals with ADPKD (the “XRX-OXY-301 Clinical Trial”). The XRX-OXY-301 Clinical Trial is a Phase 3, Multi-Centre, Double-Blind, Placebo Controlled, Randomized Withdrawal Design Study to Evaluate the Efficacy and Safety of a Novel Oxypurinol Formulation in Patients with Progressing Stage 2-4 ADPKD and Coexistent Hyperuricemia. XORTX anticipates that the XRX-OXY-301 Clinical Trial will provide data to support submission of a future NDA application for “Accelerated Approval” to the FDA and Marketing Authorization Application to the European Medicines Agency “EMA.” The XRX-OXY-301 Clinical Trial is planned, subject to additional financing, to start in the second half of 2023 and will enroll individuals with stage 2, 3 or 4 ADPKD accompanied by chronically high uric acid. The objective of the XRX-OXY-301 Clinical Trial is to evaluate the ability of XORLOTM to slow the expansion of total kidney volume over a 12-month treatment period. FDA has granted Orphan Drug Designation status for XRx-008, and confirmation that this program is eligible for Accelerated Approval when Total Kidney Volume (TKV) or estimated glomerular filtration rate (eGFR) clinical data are produced after a 1 year treatment period. |

| 2. | Prepare and Communicate with the FDA and EMA regarding the XRX-OXY-302 Registration trial in ADPKD (the “XRX-OXY-302 Clinical Trial”). The XRX-OXY-302 Clinical Trial is a Phase 3, Multi-Centre, Double-Blind, Placebo Controlled, Randomized Withdrawal Design Study to Evaluate the Efficacy and Safety of a Novel Oxypurinol Formulation in Patients with Progressing Stage 2-4 ADPKD and Coexistent Hyperuricemia with progressing stage 2, 3, or 4 kidney disease. The objective of the XRX-OXY-302 Clinical Trial is to evaluate the safety and effectiveness of XORLOTM for the XRx-008 program over a 24-month treatment period. The aim of the XRX-OXY-302 Clinical Trial is to characterize the ability of xanthine oxidase inhibitors to potentially decrease the rate of decline of glomerular filtration rate. An estimated 300 patients will be enrolled. The XRX-OXY-302 Clinical Trial is planned to start in the second half of 2024, subject to Special Protocol Assessment review by FDA. |

| 3. | Ongoing Chemistry Manufacturing and Control (“CMC”) Work. In parallel with the XRX-OXY-301 and XRX-OXY-302 Clinical Trials, XORTX will be focusing on scale-up, validation and stability testing of clinical drug product supplies of XORLOTM under the Company’s investigational new drug application, as well as future clinical and commercial supplies. All development will be performed according to current Good Manufacturing Practices methodology. This work will be ongoing throughout 2023. |

| 4. | Activities Related to Potential Commercial Launch. In preparation for a possible “Accelerated Approval” NDA filing and approval in 2025 in the US for XORLOTM XRx-008, XORTX will conduct pre-commercialization studies to support in-depth analysis of pricing and/or reimbursement, as well as evaluate product brand name selection, prepare related filings, and conduct other launch preparation activities. This work will be ongoing from 2023 to 2025. |

| 5. | Activities Related to European Registration. XORTX will continue to work with and seek out guidance from the EMA to facilitate the path to potential approval of XORLOTM in the European Union (“EU”), including required clinical studies and reimbursement conditions. This work will be ongoing from 2023 through 2026 and will include a future request for orphan drug status. XORTX intends to seek EMA Orphan Drug Designation status in 2023 to 2024. |

To achieve the above goals, XORTX will continue to pursue non-dilutive and dilutive funding and expand discussions to partner with pharma / biotech companies with a global reach. XORTX will also increase financial and healthcare conference participation to further strengthen and expand its investor base.

Recent Developments

On June 29, 2023, the Company announced the appointment of James Fairbairn as Interim Chief Financial Officer (“CFO”).

FDA has granted Orphan Drug Designation status to XRx-008.

Risk Factors

Our ability to implement our business strategy is subject to numerous risks that you should be aware of before making an investment decision. These risks are described more fully in the sections entitled “Risk Factors” in this prospectus and under “Risk Factors Summary” and “Item 3. Key Information—D. Risk Factors” in our Annual Report on Form 20-F for the year ended December 31, 2022, incorporated by reference herein.

Our Corporate Information

We were incorporated under the laws of Alberta, Canada on August 24, 2012, under the name ReVasCor Inc. and were continued under the Canada Business Corporations Act on February 27, 2013, under the name of XORTX Pharma Corp. Upon completion of a reverse take-over transaction on January 10, 2018, with APAC Resources Inc., a company incorporated under the laws of British Columbia, we changed our name to “XORTX Therapeutics Inc.” and XORTX Pharma Corp. became a wholly-owned subsidiary.

4

Our registered office is located at 3710 – 33rd Street NW, Calgary, Alberta, Canada T2L 2M1 and our telephone number is (403) 455-7727. Our website address is www.xortx.com. The information contained on, or that can be accessed through, our website is not a part of this prospectus. We have included our website address in this prospectus solely as an inactive textual reference.

Implications of Being an Emerging Growth Company

As a company with less than $1.235 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other burdens that are otherwise applicable generally to public companies. These provisions include:

| · | reduced executive compensation disclosure; |

| · | exemptions from the requirement to hold a non-binding advisory vote on executive compensation, including golden parachute compensation; and |

| · | an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002. |

We may take advantage of these provisions until we are no longer an emerging growth company. We would cease to be an emerging growth company upon the earlier to occur of: (1) the last day of our fiscal year following the fifth anniversary of the completion of this offering; (2) the last day of the fiscal year in which we have total annual gross revenue of $1.235 billion or more; (3) the date on which we have issued more than $1.0 billion in nonconvertible debt during the previous three years; or (4) the date on which we are deemed to be a large accelerated filer under the rules of the SEC. We have elected not to take advantage of the extended transition period allowed for emerging growth companies for complying with new or revised accounting guidance as allowed by Section 107 of the JOBS Act and Section 7(a)(2)(B) of the Securities Act.

5

We report under the Securities Exchange Act of 1934, as amended (“Exchange Act”), as a non-U.S. company with foreign private issuer status. Even after we no longer qualify as an emerging growth company, as long as we continue to qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| · | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations with respect to a security registered under the Exchange Act; |

| · | the sections of the Exchange Act requiring insiders to file public reports of their share ownership and trading activities and liability for insiders who profit from trades made in a short period of time; and |

| · | the rules under the Exchange Act requiring the filing with the SEC of quarterly reports on Form 10-Q containing unaudited financial statements and other specified information, and current reports on Form 8-K upon the occurrence of specified significant events, although we report our results of operations on a quarterly basis under the Canadian securities laws. |

Both foreign private issuers and emerging growth companies are also exempt from certain more stringent executive compensation disclosure rules. Thus, even if we no longer qualify as an emerging growth company, but remain a foreign private issuer, we will continue to be exempt from the more stringent compensation disclosures required of companies that are neither an emerging growth company nor a foreign private issuer.

We would cease to be a foreign private issuer at such time as more than 50% of our outstanding voting securities are held by U.S. residents, and any one of the following three circumstances applies: (i) the majority of our executive officers or directors are U.S. citizens or residents, (ii) more than 50% of our assets are located in the United States or (iii) our business is administered principally in the United States.

In this prospectus, we have taken advantage of certain of the reduced reporting requirements as a result of being an emerging growth company and a foreign private issuer. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you hold equity securities.

6

The Offering

Securities offered |

Up to 5,000,000 common shares, no par value per share (each a “common share”) are issuable upon exercise of the Warrants at an exercise price per common share of $1.22. | |

| Description of Warrants | The Warrants were offered and sold by us pursuant to a prospectus dated October 4, 2022, as part of a public offering of common share units and pre-funded warrant units. The common share units consisted of 1,400,000 common shares and Warrants to purchase up to 1,400,000 common shares. The pre-funded warrant units consisted of 3,600,000 pre-funded warrants and Warrants to purchase up to 3,600,000 common shares. The common shares and Warrants were immediately separable upon issuance. Each common share unit was sold at a price of $1.00 per common share unit. Each pre-funded warrant unit was sold at a price of $0.9999 and had an exercise price of $0.0001. The Warrants sold in the offering have an exercise price of $1.22 and expire five years from the original date of issuance (October 7, 2027). | |

| Limitations on beneficial ownership | Under the Warrants, a holder (together with its affiliates) may not exercise any portion of a Warrant to the extent that the holder would own more than 4.99% of our outstanding common shares outstanding immediately after exercise, except that upon at least 61 days’ prior notice from the holder to us, the holder may increase the amount of ownership of outstanding common shares after exercising the holder’s Warrants up to 9.99% of the number of our common shares outstanding immediately after giving effect to the exercise, as such percentage ownership is determined in accordance with the terms of the Warrants. | |

| Common shares to be outstanding after this offering, assuming exercise of all of the Warrants | 22,989,687 shares | |

| Use of proceeds | We may receive proceeds from the exercise of the warrants if exercised for cash, but not from the sale of the underlying common shares. We intend to use the net proceeds of the warrant exercises to fund our ongoing research and development activities, and for working capital and general corporate purposes. See “Use of Proceeds”. | |

| Nasdaq trading symbol | “XRTX” | |

| No Listing of Warrants | We do not intend to apply for listing of the Warrants on any national securities exchange or trading system. | |

| Risk Factors | Please refer to “Risk Factors” in this prospectus and under “Risk Factors Summary” and “Item 3. Key Information—D. Risk factors” in our Annual Report on Form 20-F for the year ended December 31, 2022, incorporated by reference herein, and other information included or incorporated by reference in this prospectus for a discussion of factors you should carefully consider before investing in our common shares. |

7

The number of common shares to be outstanding after this offering is based on 17,989,687 common shares outstanding as of March 31, 2023, and excludes:

| · | 1,039,335 common shares issuable upon the exercise of outstanding options to issue common shares, as of March 31, 2023, at a weighted average exercise price of CAD$2.03 per common share; and |

| · | 5,579,796 common shares issuable upon the exercise of outstanding common share warrants (excluding the Warrants), as of March 31, 2023, at a weighted-average exercise price of $3.59 per common share. |

Unless otherwise indicated, all information in this prospectus reflects or assumes the Warrants have all been exercised.

8

On June 29, 2023, we announced the appointment of James Fairbairn as Interim CFO. On July 31, 2023, Amar Keshri ceased to be employed by the Company.

Pursuant to Mr. Fairbairn’s appointment as our interim CFO, we entered into a consulting agreement with 1282803 Ontario Inc., pursuant to which we appointed Mr. Fairbairn to act as our consultant, including in the capacity as our interim CFO (the “Fairbairn Consulting Agreement”). The terms of the Fairbairn Consulting Agreement are effective from July 3, 2023 on a continuous basis until terminated by either party and provided for Mr. Fairbairn’s services as an independent consultant. Under the Fairbairn Consulting Agreement, Mr. Fairbairn will act as our CFO for a term of one-year, which shall automatically renew, but is cancellable by either party on 90 days’ notice. In return for services as Interim CFO, we will pay a fee of CAD$205,540 annually. In addition, Mr. Fairbairn is to provide certain strategic financial guidance for a one-year term in exchange for the grant of 30,000 stock options, which shall vest equally over 36 months. The Fairbairn Consulting Agreement provides that Mr. Fairbairn is eligible to participate in our stock option plan and is eligible for a discretionary bonus of up to 30% of the annual base consulting fees. Either party may terminate the Fairbairn Consulting Agreement upon not less than 30 days written notice. In the event that we were to terminate the agreement, we would be required to pay a single lump-sum termination payment equal to one month of the base consulting fee as in effect at the time of termination.

9

Any investment in our securities involves a high degree of risk. You should carefully consider the risks described below and in “Risk Factors Summary” and “Item 3. Key Information - D. Risk factors” in our Annual Report on Form 20-F for the year ended December 31, 2022, incorporated by reference herein, and all of the information included or incorporated by reference in this prospectus before deciding whether to purchase our securities. The risks and uncertainties described below are not the only risks and uncertainties we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business operations. If any of the events or circumstances described in the following risk factors actually occur, our business, financial condition and results of operations would suffer. In that event, the price of our common shares could decline, and you may lose all or part of your investment. The risks discussed below also include forward-looking statements and our actual results may differ substantially from those discussed in these forward-looking statements. See “Cautionary Note Regarding Forward-Looking Statements.”

Risks Related to this Offering

We will have broad discretion in how we use the proceeds, and we may use the proceeds in ways in which you and other stockholders may disagree.

We intend to use the net proceeds we receive from this offering, if any, to fund our ongoing research and development activities, and for working capital and general corporate purposes. Our management will have broad discretion in the application of the proceeds from this offering and could spend the proceeds in ways that do not necessarily improve our operating results or enhance the value of our common shares.

If you purchase common shares in this offering by exercising warrants, you will suffer immediate dilution of your investment.

The public offering price of our common shares is substantially higher than the as adjusted net tangible book value per common share. Therefore, if you purchase common shares in this offering by exercising warrants, you will pay a price per common share that substantially exceeds our as adjusted net tangible book value per common share after this offering. To the extent outstanding options are exercised, you will incur further dilution. Based on the exercise price per common share of the Warrants, you will experience immediate dilution of $0.57 per common share, representing the difference between our as adjusted net tangible book value per common share after giving effect to this offering and the applicable exercise price. See “Dilution.”

10

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this Annual Report constitute forward-looking statements. These statements relate to future events or the Company’s (as defined herein) future performance. All statements other than statements of historical fact are forward-looking statements. The use of any of the words “anticipate”, “plan”, “contemplate”, “continue”, “estimate”, “expect”, “intend”, “propose”, “might”, “may”, “will”, “shall”, “project”, “should”, “could”, “would”, “believe”, “predict”, “forecast”, “pursue”, “potential” and “capable” and similar expressions are intended to identify forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. No assurance can be given that these expectations will prove to be correct and such forward-looking statements included in this Annual Report should not be unduly relied upon. These statements speak only as of the date of this Annual Report. In addition, this Annual Report may contain forward-looking statements and forward-looking information attributed to third party industry sources.

In particular, forward-looking statements in this Annual Report include, but are not limited to, statements about:

| · | our ability to obtain additional financing; |

| · | the accuracy of our estimates regarding expenses, future revenues and capital requirements; |

| · | the success and timing of our preclinical studies and clinical trials; |

| · | our ability to obtain and maintain regulatory approval of XRx-008, also sometimes referred to by its trademarked name XORLOTM. XORTX’s proprietary formulation of oxypurinol, and any other product candidates we may develop, and the labeling under any approval we may obtain; |

| · | regulatory approvals and discussions and other regulatory developments in the United States, the EU and other countries; |

| · | the performance of third-party manufacturers and contract research organizations; |

| · | our plans to develop and commercialize our product candidates, if approved; |

| · | our plans to advance research in other kidney disease applications; |

| · | our ability to obtain and maintain intellectual property protection for our product candidates; |

| · | the successful development of our sales and marketing capabilities; |

| · | the potential markets for our product candidates and our ability to serve those markets; |

| · | the rate and degree of market acceptance of any future products; |

| · | the success of competing drugs that are or become available; and |

| · | the loss of key scientific or management personnel. |

All forward-looking statements, including, without limitation, our examination of historical operating trends, are based upon our current expectations and various assumptions. Certain assumptions made in preparing the forward-looking statements include:

| · | the availability of capital to fund planned expenditures; |

| · | prevailing regulatory, tax and environmental laws and regulations; |

| · | the ability to secure necessary personnel, equipment, supplies and services; |

| · | our ability to manage our growth effectively; |

| · | the absence of material adverse changes in our industry or the global economy; |

| · | trends in our industry and markets; |

11

| · | our ability to maintain good business relationships with our strategic partners; |

| · | our ability to comply with current and future regulatory standards; |

| · | our ability to protect our intellectual property rights; |

| · | our continued compliance with third-party license terms and the non-infringement of third-party intellectual property rights; |

| · | our ability to manage and integrate acquisitions; and |

| · | our ability to raise sufficient debt or equity financing to support our continued growth. |

We believe there is a reasonable basis for our expectations and beliefs, but they are inherently uncertain. We may not realize our expectations, and our beliefs may not prove correct. Actual results could differ materially from those described or implied by such forward-looking statements.

12

We express all amounts in this prospectus in United States dollars, except where otherwise indicated. References to “$” are to United States dollars and references to “CAD$” are to Canadian dollars. The following table sets forth, for the periods indicated, average rate of exchange for one U.S. dollar, expressed in Canadian dollars, for the years ended December 31, 2022, 2021 and 2020, as supplied by the Bank of Canada:

| Year Ended | Average | |||

| December 31, 2022 | 1.3013 | |||

| December 31, 2021 | 1.2535 | |||

| December 31, 2020 | 1.3415 | |||

On June 30, 2023, the Bank of Canada average daily rate of exchange was $1.00 = CAD$1.3240.

13

MARKET, INDUSTRY AND OTHER DATA

Unless otherwise indicated, information contained in, and incorporated into, this prospectus concerning our industry and the market in which we operate, including our market position, market opportunity and market size, is based on information from various third-party sources not prepared at the direction of the Company, such as industry publications, and assumptions that we have made based on such data and other similar sources and on our knowledge of the markets for our products. These data involve a number of assumptions and limitations. We believe that this data is accurate and that its estimates and assumptions are reasonable, but there can be no assurance as to the accuracy or completeness of this data. We have not independently verified any of the data from third-party sources referred to in, or incorporated into, this prospectus or analyzed or verified the underlying studies or surveys relied upon or referred to by such sources, or ascertained the underlying economic assumptions relied upon or referred to by such sources.

In addition, projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate is necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section entitled “Risk Factors” and discussed elsewhere in this prospectus, as well as in “Risk Factors Summary” and “Item 3. Key Information - D. Risk factors” in our Annual Report on Form 20-F for the year ended December 31, 2022, incorporated by reference herein. These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

14

To the extent that the Warrants are exercised for cash, we will receive the gross cash proceeds from such exercise of up to a total potential of approximately $6,100,000 million, based on the current exercise price of the Warrants. We cannot predict when or if any of the Warrants will be exercised, and it is possible that the warrants may expire and never be exercised.

We intend to use the net proceeds from the issuance of the securities for working capital and general corporate purposes. Such purposes may include research and development expenditures and capital expenditures.

Our management will have broad discretion in the application of the net proceeds of this offering, and investors will be relying on our judgment regarding the application of the net proceeds. In addition, we might decide to postpone or not pursue certain preclinical activities or clinical trials if the net proceeds from this offering and our other sources of cash are less than expected.

Pending their use, we plan to invest the net proceeds of any Warrant exercises in short-and intermediate-term interest-bearing investments.

15

We have never paid any dividends on our common shares or any of our other securities. We currently intend to retain any future earnings to finance the growth and development of our business, and we do not anticipate that we will declare or pay any cash dividends in the foreseeable future. Any future determination to pay cash dividends will be at the discretion of our Board of Directors and will be dependent upon our financial condition, results of operations, capital requirements, restrictions under any future indebtedness and other factors the Board of Directors deems relevant.

16

CAPITALIZATION AND INDEBTEDNESS

The following table sets forth our cash as well as capitalization as of March 31, 2023:

| · | on an actual basis; |

| · | on an as adjusted basis to give effect to our issuance of 5,000,000 common shares offered hereby upon exercise of the Warrants at an exercise price per common share of $1.22; |

| · | Canadian Dollar amounts have been translated into U.S. Dollars based on the March 31, 2023, daily rate of exchange, which was $1.00 = CAD$1.3533 or CAD$1.00 = $0.7389 as reported by the Bank of Canada and have been provided solely for the convenience of the reader. |

You should read this table together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in “Item 5. Operating and Financial Review and Prospects” and our financial statements and related notes thereto included in “Item 18. Financial Statements” included in our Annual Report on Form 20-F for the year ended December 31, 2022, incorporated by reference herein.

| As of March 31, 2023 | ||||||||

| Pro forma as | ||||||||

| Actual | adjusted | |||||||

| (In thousands, except share data) | ||||||||

| Cash | $ | 7,908 | $ | 14,008 | ||||

| Equity | ||||||||

| Share capital | $ | 17,057 | $ | 23,157 | ||||

| Common shares, unlimited authorized shares, without par value; 17,989,687 shares issued and outstanding, actual; 22,989,687 shares issued and outstanding, pro forma as adjusted | ||||||||

| Share-based payments, warrant reserve and other | $ | 9,559 | $ | 9,559 | ||||

| Obligation to Issue Shares | $ | 25 | $ | 25 | ||||

| Accumulated other comprehensive (loss) income | $ | (53 | ) | $ | (53 | ) | ||

| Deficit | $ | (17,529 | ) | $ | (17,529 | ) | ||

| Total Equity | $ | 9,059 | $ | 15,159 | ||||

| Total Capitalization | $ | 9,059 | $ | 15,159 | ||||

The number of common shares to be outstanding after this offering is based on an aggregate of 17,989,687 shares outstanding as of March 31, 2023. The table above excludes:

| · | 1,039,335 common shares issuable upon the exercise of outstanding options to issue common shares, as of March 31, 2023, at a weighted-average exercise price of CAD$2.03 per share; and | |

| · | 5,579,796 common shares issuable upon the exercise of outstanding common share purchase warrants, as of March 31, 2023, at a weighted-average exercise price of $3.59 per share. |

For additional information regarding our share capital and the terms of the Warrants, see “Description of Share Capital” and “Description of Warrants.”

17

If you exercise Warrants in this offering for our common shares, your interest will be diluted to the extent of the difference between the price per common share you will pay and the as adjusted net tangible book value per common share after the exercise.

As of March 31, 2023, we had a net tangible book value of $8,890 million, corresponding to a net tangible book value of $0.49 per common share. Net tangible book value per share represents the amount of our total assets less our total liabilities, excluding intangible assets, divided by 17,989,687, the total number of our common shares outstanding as of March 31, 2023.

Assuming that we issue 5,000,000 common shares upon exercise of the Warrants at an exercise price per common share of $1.22, our as adjusted net tangible book value estimated as of March 31, 2023 would have been $14,991 million, representing $0.65 per common share. This represents an immediate increase in net tangible book value of $0.16 per common share to existing shareholders and an immediate dilution in net tangible book value of $0.57 per common share to new investors acquiring common shares upon the exercise of the Warrants. Dilution for this purpose represents the difference between the exercise price per common share paid upon exercise of the Warrants and net tangible book value per common share immediately after the exercise.

The following table illustrates this dilution to new investors for holders of Warrants.

| Warrant holder |

||||

| Exercise price per common share | $ | 1.22 | ||

| Net tangible book value per common share as of March 31, 2023 | $ | 0.49 | ||

| Increase in net tangible book value per common share attributable to new investors | $ | 0.16 | ||

| As adjusted net tangible book value per common share after the exercise | $ | 0.65 | ||

| Dilution per common share to new investors | $ | 0.57 | ||

| Percentage of dilution in net tangible book value per common share for new investors | 46.72 | % | ||

The above discussion and table are based on 17,989,687 common shares outstanding as of March 31, 2023, and excludes:

| · | 1,039,335 common shares issuable upon the exercise of outstanding options to issue common shares, as of March 31, 2023, at a weighted-average exercise price of CAD$2.03 per share; and | |

| · | 5,579,796 common shares issuable upon the exercise of outstanding common share purchase warrants, as of March 31, 2023, at a weighted-average exercise price of $3.59 per share. |

To the extent that outstanding options or warrants are exercised, you may experience further dilution. In addition, we may choose to raise additional capital due to market conditions or strategic considerations even if we believe we have sufficient funds for our current or future operating plans. To the extent that additional capital is raised through the sale of equity or convertible debt securities, the issuance of these securities may result in further dilution to our shareholders.

Canadian Dollar amounts have been translated into U.S. Dollars based on the March 31, 2023, daily rate of exchange, which was $1.00 = CAD$1.3533 or CAD$1.00 = $0.7389 as reported by the Bank of Canada and have been provided solely for the convenience of the reader.

18

Our common shares are listed on Nasdaq and the TSXV under the symbol “XRTX”.

TRANSFER AGENT, REGISTRAR AND AUDITOR

The transfer agent and registrar for our common shares is TSX Trust Company at its principal office in Toronto, Canada. Our co-transfer agent is Continental Stock Transfer & Trust Company.

Smythe LLP, located at 1700 — 475 Howe Street, Vancouver, British Columbia, Canada V6C 2B3 is our independent registered public accounting firm and has been appointed as our independent auditor.

19

General

The following is a summary of the material rights of our share capital as contained in our notice of articles and articles and any amendments thereto. This summary is not a complete description of the share rights associated with our capital stock. For more detailed information, please see our notice of articles and articles, which are filed as exhibits to the registration statement of which this prospectus forms a part.

Common Shares

Outstanding Shares

Our authorized share capital consists of an unlimited number of common shares, each without par value.

As of March 31, 2023, we had 795,859 common shares issuable pursuant to exercisable outstanding stock options, 243,476 common shares issuable pursuant to outstanding options that are not currently exercisable, 10,579,796 common shares issuable upon the exercise of outstanding common share warrants, and we had approximately 15 holders of record of our common shares.

Voting Rights

Under our articles, the holders of our common shares are entitled to one vote for each common share held on all matters submitted to a vote of the shareholders, including the election of directors. Our notice of articles and articles do not provide for cumulative voting rights. Because of this, the holders of a plurality of the common shares entitled to vote in any election of directors can elect all of the directors standing for election, if they so choose.

Dividends

Subject to priority rights that may be applicable to any then outstanding common shares, and the applicable provisions of the Business Corporation Act British Columbia (“BCBCA”), holders of our common shares are entitled to receive dividends, as and when declared by our Board, in their sole discretion as they see fit. For more information, see the section titled “Dividend Policy.”

Liquidation

In the event of our liquidation, dissolution or winding up, holders of our common shares are entitled to share ratably in the net assets legally available for distribution to shareholders after the payment of all of our debts and other liabilities and the satisfaction of any liquidation preference granted to the holders of any then outstanding preferred shares.

Rights and Preferences

Our common shares contain no pre-emptive or conversion rights and have no provisions for redemption or repurchase for cancellation, surrender or sinking or purchase funds. There are no provisions in our notice of articles and articles requiring holders of common shares to contribute additional capital. The rights, preferences and privileges of the holders of our common shares are subject to and may be adversely affected by the rights of the holders of any series of new preferred shares that may be created, authorized, designated, and issued in the future.

Fully Paid and Non-assessable

All of our outstanding common shares are, and the common shares to be issued pursuant to this Prospectus, when paid for, will be fully paid and non-assessable.

20

The following is a summary of certain terms and provisions of the Warrants. This summary is not complete and is subject to, and qualified in its entirety by, the provisions of the Warrants, the form of which is included as exhibit 4.6 to the registration statement of which this prospectus forms a part. Prospective investors should carefully review the terms and provisions of the form of Warrants for a complete description of the terms and conditions of the Warrants.

Duration and Exercise Price

Each Warrant included had an initial exercise price equal to $1.22 per common share.

The Warrants were immediately exercisable and expire on the fifth anniversary of the original issuance date (October 7, 2027). The exercise price and number of common shares issuable upon exercise is subject to appropriate adjustment in the event of share dividends, share splits, reorganizations or similar events affecting our common shares and the exercise price. The Warrants were sold in common share units and pre-funded warrant units, with the common share unit consisting of one common share and one Warrant and each pre-funded warrant unit consisting of one pre-funded warrant and one Warrant.

Cashless Exercise

If, at the time a holder exercises its Warrants, a registration statement registering the issuance of the shares of common shares underlying the under the Securities Act is not then effective or available for the issuance of such shares, then in lieu of making the cash payment otherwise contemplated to be made to us upon such exercise in payment of the aggregate exercise price, the holder may elect instead to receive upon such exercise (either in whole or in part) the net number of common shares determined according to a formula set forth in the Warrants.

Exercisability

The Warrants are exercisable, at the option of each holder, in whole or in part, by delivering to us a duly executed exercise notice accompanied by payment in full for the number of common shares purchased upon such exercise (except in the case of a cashless exercise as discussed below). A holder (together with its affiliates) may not exercise any portion of the Warrant to the extent that the holder would own more than 4.99% of the outstanding common shares immediately after exercise, except that upon at least 61 days’ prior notice from the holder to us, the holder may increase the amount of ownership of outstanding common shares after exercising the holder’s Warrants up to 9.99% of the number of common shares outstanding immediately after giving effect to the exercise, as such percentage ownership is determined in accordance with the terms of the Warrants. Purchasers of Warrants in the 2021 public offering could also elect, prior to the issuance of the Warrants, to have the initial exercise limitation set at 9.99% of our outstanding common shares.

Fractional Shares

No fractional common shares will be issued upon the exercise of the Warrants. Rather, the number of common shares to be issued will be rounded up to the nearest whole number, or the Company shall pay a cash adjustment in respect of the fractional share.

Transferability

Subject to applicable laws, the Warrants may be offered for sale, sold, transferred or assigned without our consent. There is currently no trading market for the Warrants.

Exchange Listing

There is no trading market available for the Warrants on any securities exchange or nationally recognized trading system. We do not intend to list the Warrants on any securities exchange or nationally recognized trading system.

Right as a Shareholder

Except as otherwise provided in the Warrants or by virtue of such holder’s ownership of common shares, the holders of the Warrants do not have the rights or privileges of holders of our common shares, including any voting rights, until they exercise their Warrants.

Fundamental Transaction

In the event of a fundamental transaction, as described in the Warrants and generally including any reorganization, recapitalization or reclassification of our common shares, the sale, transfer or other disposition of all or substantially all of our properties or assets, our consolidation or merger with or into another person, the acquisition of more than 50% of our outstanding common shares, or any person or group becoming the beneficial owner of 50% of the voting power represented by our outstanding common shares, the holders of the Warrants will be entitled to receive upon exercise of the Warrants the kind and amount of securities, cash or other property that the holders would have received had they exercised the Warrants immediately prior to such fundamental transaction.

21

Material Canadian Federal Income Tax Considerations

The following is, as of the date of this prospectus, a general summary of the principal Canadian federal income tax considerations under the Income Tax Act (Canada), or the Canadian Tax Act, generally applicable to an investor who acquires common share units pursuant to this offering and who, for the purposes of the Canadian Tax Act and at all relevant times, deals at arm’s length with the Company and the underwriters, is not affiliated with the Company or the underwriters and who acquires and holds the common shares, or Warrants as capital property, or a Holder. Generally, the common shares and Warrants will be considered to be capital property to a Holder thereof provided that the Holder does not use the common shares in the course of carrying on a business of trading or dealing in securities and such Holder has not acquired them in one or more transactions considered to be an adventure or concern in the nature of trade.

This summary does not apply to a Holder (i) that is a “financial institution” for the purposes of the mark-to-market rules contained in the Canadian Tax Act; (ii) that is a “specified financial institution” as defined in the Canadian Tax Act; (iii) if an interest in such a Holder is a “tax shelter” or a “tax shelter investment,” each as defined in the Canadian Tax Act; (iv) a holder that reports its “Canadian tax results,” as defined in the Canadian Tax Act, in a currency other than Canadian currency; or (v) that has or will enter into a “derivative forward agreement” or a “synthetic disposition arrangement”, as those terms are defined in the Canadian Tax Act, with respect to the common shares and Warrants. Such Holders should consult their own tax advisors with respect to the consequences of acquiring common share units.

Additional considerations, not discussed herein, may be applicable to a Holder that (i) is a corporation resident in Canada and (ii) is (or does not deal at arm’s length for the purposes of the Canadian Tax Act with a corporation resident in Canada that is), or becomes as part of a transaction or event or series of transactions or events that includes the acquisition of the common share units, controlled by a corporation that is not resident in Canada for purposes of the “foreign affiliate dumping” rules in section 212.3 of the Canadian Tax Act. Such Holders should consult their own tax advisors with respect to the consequences of acquiring common share units.

This summary is based upon the current provisions of the Canadian Tax Act and the regulations thereunder, or the Regulations, in force as of the date hereof and the Company’s understanding of the current published administrative and assessing practices of the Canada Revenue Agency, or the CRA. This summary takes into account all specific proposals to amend the Canadian Tax Act and the Regulations publicly announced by or on behalf of the Minister of Finance (Canada) prior to the date hereof, or the Tax Proposals, and assumes that the Tax Proposals will be enacted in the form proposed, although no assurance can be given that the Tax Proposals will be enacted in their current form or at all. This summary does not otherwise take into account any changes in law or in the administrative policies or assessing practices of the CRA, whether by legislative, governmental or judicial decision or action, nor does it take into account or consider any provincial, territorial or foreign income tax considerations, which considerations may differ significantly from the Canadian federal income tax considerations discussed in this summary.

This summary is of a general nature only, is not exhaustive of all possible Canadian federal income tax considerations and is not intended to be, nor should it be construed to be, legal or tax advice to any particular Holder. This summary does not address the deductibility of interest expense incurred or paid by a Holder that has borrowed money in connection with the acquisition of common share units pursuant to this offering. Holders should consult their own tax advisors with respect to their particular circumstances.

All amounts in a currency other than the Canadian dollar relevant in computing a Holder’s liability under the Canadian Tax Act with respect to the acquisition, holding or disposition of common shares and Warrants must generally be converted into Canadian dollars using the single daily exchange rate quoted by the Bank of Canada for the day on which the amount arose or such other rate of exchange that is acceptable to the CRA.

22

Residents of Canada

The following section of this summary applies to a Holder who, for the purposes of the Canadian Tax Act, is or is deemed to be resident in Canada at all relevant times, or a Canadian Resident Holder. Certain Canadian Resident Holders whose common shares might not constitute capital property may in certain circumstances make an irrevocable election in accordance with subsection 39(4) of the Canadian Tax Act to deem the common shares, and every other “Canadian security” as defined in the Canadian Tax Act, held by such Canadian Resident Holder, in the taxation year of the election and each subsequent taxation year to be capital property. Canadian Resident Holders should consult their own tax advisors regarding this election.

Dividends

Dividends received or deemed to be received on the common shares will be included in computing a Canadian Resident Holder’s income. In the case of an individual (other than certain trusts), such dividends will be subject to the gross-up and dividend tax credit rules normally applicable in respect of “taxable dividends” received from “taxable Canadian corporations” (each as defined in the Canadian Tax Act). An enhanced dividend tax credit will be available to individuals in respect of “eligible dividends” designated by the Company to the Canadian Resident Holder in accordance with the provisions of the Canadian Tax Act.

Dividends received or deemed to be received by a corporation that is a Canadian Resident Holder on the common shares must be included in computing its income but generally will be deductible in computing its taxable income. In certain circumstances, subsection 55(2) of the Canadian Tax Act will treat a taxable dividend received by a Canadian Resident Holder that is a corporation as proceeds of disposition or a capital gain. A Canadian Resident Holder that is a corporation should consult its own tax advisors having regard to its own circumstances. A Canadian Resident Holder that is a “private corporation” as defined in the Canadian Tax Act and certain other corporations controlled, by or for the benefit of an individual (other than a trust) or a related group of individuals (other than trusts) generally will be liable to pay a 38 1/3% refundable tax under Part IV of the Canadian Tax Act on dividends received or deemed to be received on the common shares to the extent such dividends are deductible in computing taxable income. Such refundable tax will generally be refunded to a corporate Canadian Resident Holder at the rate of 38 1/3% of taxable dividends paid while it is a private corporation.

Expiry of Warrants

In the event of the expiry of an unexercised Warrant, a Canadian Resident Holder will be considered to have disposed of such Warrant for nil proceeds and will accordingly realize a capital loss equal to the Canadian Resident Holder’s adjusted cost base of such Warrant immediately before that time. For a description of the tax treatment of capital losses, see “Capital Gains and Losses”, below.

Exercise of Warrants

No gain or loss will be realized by a Canadian Resident Holder on the exercise of a Warrant to acquire common shares. When a Warrant is exercised, the Canadian Resident Holder’s cost of the common shares acquired thereby will be equal to the adjusted cost base of the Warrant to the Canadian Resident Holder, immediately before that time, plus the amount paid on the exercise of the Warrant. For the purpose of computing the adjusted cost base of each common share acquired on the exercise of a Warrant, the cost of such common share must be averaged with the adjusted cost base to the Canadian Resident Holder of all other common shares held as capital property immediately before the exercise of the Warrant.

Dividends received or deemed to be received by a corporation that is a Canadian Resident Holder on the common shares must be included in computing its income but generally will be deductible in computing its taxable income. In certain circumstances, subsection 55(2) of the Canadian Tax Act will treat a taxable dividend received by a Canadian Resident Holder that is a corporation as proceeds of disposition or a capital gain. A Canadian Resident Holder that is a corporation should consult its own tax advisors having regard to its own circumstances. A Canadian Resident Holder that is a “private corporation” as defined in the Canadian Tax Act and certain other corporations controlled, by or for the benefit of an individual (other than a trust) or a related group of individuals (other than trusts) generally will be liable to pay a 38 1/3% refundable tax under Part IV of the Canadian Tax Act on dividends received or deemed to be received on the common shares to the extent such dividends are deductible in computing taxable income. Such refundable tax will generally be refunded to a corporate Canadian Resident Holder at the rate of 38 1/3% of taxable dividends paid while it is a private corporation.

Dispositions of Common Shares or Warrants

Upon a disposition (or a deemed disposition) of a common share, a Canadian Resident Holder generally will realize a capital gain (or a capital loss) equal to the amount by which the proceeds of disposition of such common share, net of any reasonable costs of disposition, are greater (or are less) than the adjusted cost base of such common share to the Canadian Resident Holder. The tax treatment of capital gains and capital losses is discussed in greater detail below under the subheading “Capital Gains and Capital Losses.”

23

The adjusted cost base to a Canadian Resident Holder of a common share acquired pursuant to this offering will be averaged with the adjusted cost base of any other of the Company’s common shares held by such Canadian Resident Holder as capital property for the purposes of determining the Canadian Resident Holder’s adjusted cost base of each common share.

Capital Gains and Capital Losses

Generally, a Canadian Resident Holder is required to include in computing its income for a taxation year one-half of the amount of any capital gain (a “taxable capital gain”) realized in the year. Subject to and in accordance with the provisions of the Canadian Tax Act, a Canadian Resident Holder is required to deduct one-half of the amount of any capital loss (an “allowable capital loss”) realized in a taxation year from taxable capital gains realized in the year by such Canadian Resident Holder. Allowable capital losses in excess of taxable capital gains may be carried back and deducted in any of the three preceding taxation years or carried forward and deducted in any following taxation year against taxable capital gains realized in such year to the extent and under the circumstances described in the Canadian Tax Act.

The amount of any capital loss realized on the disposition or deemed disposition of common shares by a Canadian Resident Holder that is a corporation may be reduced by the amount of dividends received or deemed to have been received by it on such shares or shares substituted for such shares to the extent and in the circumstances specified by the Canadian Tax Act. Similar rules may apply where a Canadian Resident Holder that is a corporation is a member of a partnership or beneficiary of a trust that owns such shares or that itself is a member of a partnership of a beneficiary of a trust that owns such shares. Canadian Resident Holders to whom these rules may be relevant should consult their own tax advisors.

A Canadian Resident Holder that is throughout the relevant taxation year a “Canadian-controlled private corporation” as defined in the Canadian Tax Act may also be liable to pay an additional refundable tax on its “aggregate investment income” for the year which will include taxable capital gains. The rate of the refundable tax is 10 2/3% for taxation years beginning after 2015. Such refundable tax will generally be refunded to a corporate Canadian Resident Holder at the rate of 38 1/3% of taxable dividends paid while it is a private corporation.

Minimum Tax

Capital gains realized and dividends received by a Canadian Resident Holder that is an individual or a trust, other than certain specified trusts, may give rise to minimum tax under the Canadian Tax Act. Such Canadian Resident Holders should consult their own advisors with respect to the application of minimum tax.

Non-Residents of Canada

The following section of this summary is generally applicable to a Holder who, for the purposes of the Canadian Tax Act, and at all relevant times: (i) has not been and will not be deemed to be resident in Canada; and (ii) does not use or hold the common shares or Warrants in, or in the course of, carrying on a business, or part of a business, in Canada, each a Non-Canadian Holder. Special rules, which are not discussed in this summary, may apply to a Non-Canadian Holder that is an insurer carrying on business in Canada and elsewhere or that is an “authorized foreign bank” as defined in the Canadian Tax Act. Such a Non-Canadian Holder should consult its own tax advisors.

Dividends

Dividends on the common shares paid or credited or deemed to be paid or credited to a Non-Canadian Holder will be subject to Canadian withholding tax at the rate of 25% on the gross amount of the dividend unless such rate is reduced by the terms of an applicable tax treaty. Under the Canada-United States Income Tax Convention (1980), or the Treaty, as amended, the rate of withholding tax on dividends paid or credited to a Non-Canadian Holder who is resident in the U.S. for purposes of the Treaty, is entitled to the full benefits under the Treaty and beneficially owns the dividend, or a U.S. Holder, is generally limited to 15% of the gross amount of the dividend (or 5% in the case of a U.S. Holder that is a corporation beneficially owning at least 10% of the Company’s voting shares). Not all persons who are residents of the U.S. for purposes of the Treaty will qualify for the benefits of the Treaty. Non-Canadian Holders that are resident in the U.S. are advised to consult their tax advisors in this regard. The rate of withholding tax on dividends is also reduced under other bilateral income tax treaties or conventions to which Canada is a signatory.

24

Expiry of Warrants

In the event of the expiry of an unexercised Warrant, a Non-Canadian Holder will be considered to have disposed of such Warrant for nil proceeds and will accordingly realize a capital loss equal to the Canadian Resident Holder’s adjusted cost base of such Warrant immediately before that time. For a description of the tax treatment of capital losses, see the discussion under “Non-Residents of Canada - Disposition of Warrants, and Common Shares”, below.

Exercise of Warrants

No gain or loss will be realized by a Non-Canadian Holder on the exercise of a Warrant. When a Warrant is exercised, the Non-Canadian Holder’s cost of the common shares acquired thereby will be equal to the adjusted cost base of the Warrant, immediately before that time, plus the amount paid on the exercise of the Warrant. For the purpose of computing the adjusted cost base of each common share acquired on the exercise of a Warrant, the cost of such common share must be averaged with the adjusted cost base to the Canadian Resident Holder of all other common shares held as capital property immediately before the exercise of the Warrant.

Dispositions of Common Shares and Warrants

A Non-Canadian Holder generally will not be subject to tax under the Canadian Tax Act in respect of a capital gain realized on the disposition or deemed disposition of a common share or Warrant nor will capital losses arising therefrom be recognized under the Canadian Tax Act, unless the common share or Warrant constitutes “taxable Canadian property” to the Non-Canadian Holder thereof for purposes of the Canadian Tax Act, and the gain is not exempt from Canadian federal income tax pursuant to the terms of an applicable tax treaty.